PayPal Ads Launches as Fintechs Are Increasingly Leveraging Their Transaction Data to Sell Ads 🇺🇸

We're also covering DoNotPay's robocaller for consumers 🇺🇸, Zeffy's pay what you want pricing 🇨🇦, Russia's SWIFT Alternative 🇷🇺, Disney Branded Accounts 🇸🇬 & Kenya's tax man crypto take 🇰🇪

🇺🇸 PayPal Ads Launches as Fintechs Are Increasingly Leveraging Their Transaction Data to Sell Ads

Fintech companies are increasingly tapping into their transaction data to power ad platforms, with PayPal being the latest to jump into the game. Mark Grether, who previously led Uber’s billion-dollar ad business, announced that PayPal Ads is set to launch in time for Black Friday during Advertising Week in New York.

Leveraging data from over 400 million PayPal users, 90 million Venmo users and the 225 billion transactions processed by its merchants, PayPal’s new ad network will allow advertisers to target their ideal clients more precisely and to measure conversions more effectively by handling the whole customer journey, from seeing an ad for a product to paying for it. Initially, ads will run PayPal owned properties such as PayPal, Venmo and Honey. However, starting next year, PayPal Ads will expand to its network of more than 30 millions merchants.

This follows a growing trend where fintech firms like Klarna and Revolut are developing their own ad network to capitalize on their vast transactions data troves. Modeled after Retail Media Networks (RMN) that have emerged from retail giants Walmart and Amazon, that allow anyone to display ads in their marketplace and leverage their transactions data, the industry calls those ad networks launched by financial firms Financial Media Networks (FMNs). According to emarketer, ad spend on these networks will quadruple in the next two years on those networks to reach 1.5 billion USD in 2026.

This rising importance of fintech data in advertising is driven by the decline of third-party cookies, increased privacy regulations around the world and limitations imposed by private platforms such as Apple that makes it harder for advertisers to track users online. Tech entrepreneur James Borow summarized this shift from behavioural ad networks like Google and Facebook to ad networks powered by transaction data in a recent post on X: “Payments are the new cookies (no matter what @Google says about them) and @Shopify has one of the best hands to play in ads as a result. Case in point - Shop Campaigns can now optimize to win back past customers, with targeted CAC and ROAS. “

Companies that have access to transaction data indeed have an increasing competitive edge in targeting consumers. Amazon, with $46.9 billion in ad revenue in 2023, exemplifies how companies with robust transaction data are thriving. Shopify, whose e-commerce and payment platform power no less than 4 millions online stores, keep refining its ad network called Shopify Audiences and recently started allowing advertisers to exclude current customers from their campaigns’ target audiences. Unlike Walmart and Amazon, however, Shopify relies on third party networks including Facebook, TikTok, Pinterest and Google to display ads, but use its transaction data to allow for improved targeting.

While Google can rely on transaction data from Google Pay and have been buying transactions data directly from Mastercard for years, it’s obvious that fintech companies will play an increasingly important role in the advertising value chain.

As someone who launched a fintech relying on transaction data to recommend financial products, I’ve been expecting this shift for a while. Companies with logged-in users and transaction histories hold a powerful advantage. PayPal, Klarna, Shopify and Revolut are just the beginning, and I would be surprised if the likes of Stripe or Adyen didn’t launch an ad network of their own at some point.

Source: Global Fintech Insider

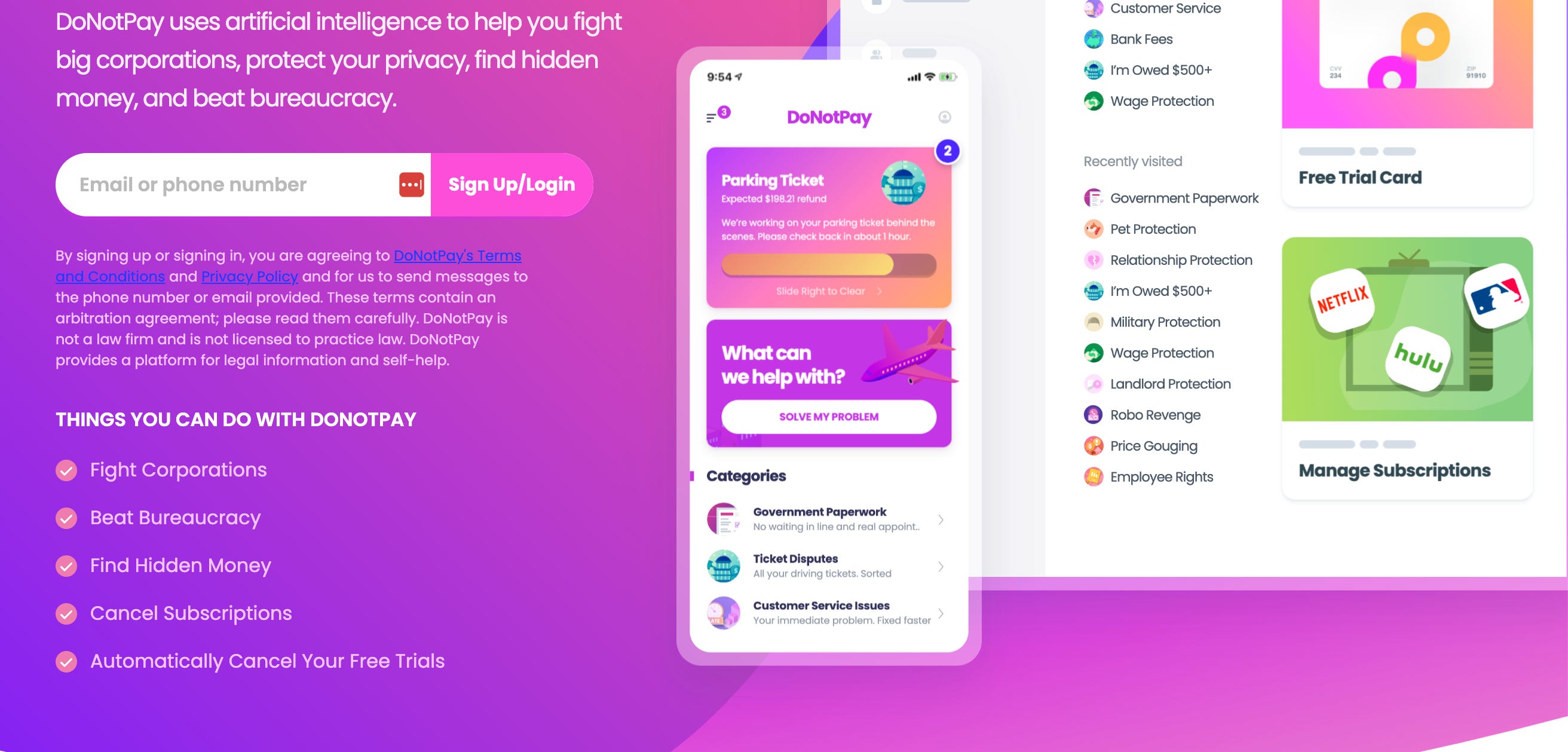

🇺🇸 DoNotPay Want to Make Hold Music A Thing of the Past Thanks to Its Robocaller For Consumers

DoNotPay, a platform originally designed to help users save money by challenging bills, cancelling subscriptions, and drafting complaint letters, has now introduced an AI-powered tool that can make customer service calls on their behalf. Leveraging OpenAI’s GPT-4o model, this bot can navigate phone menus, wait on hold, and even negotiate with customer service agents to resolve issues like flight cancellations or getting a discount on a utility bill. "The latency in foundation models has decreased by over 70%, allowing for passable customer service phone calls", explained Joshua Browder, CEO of DoNotPay, in a Linkedin post. Priced at $18 per month, the service unfortunately does not allow its users to call government agencies.

Sources: Global Fintech Insider

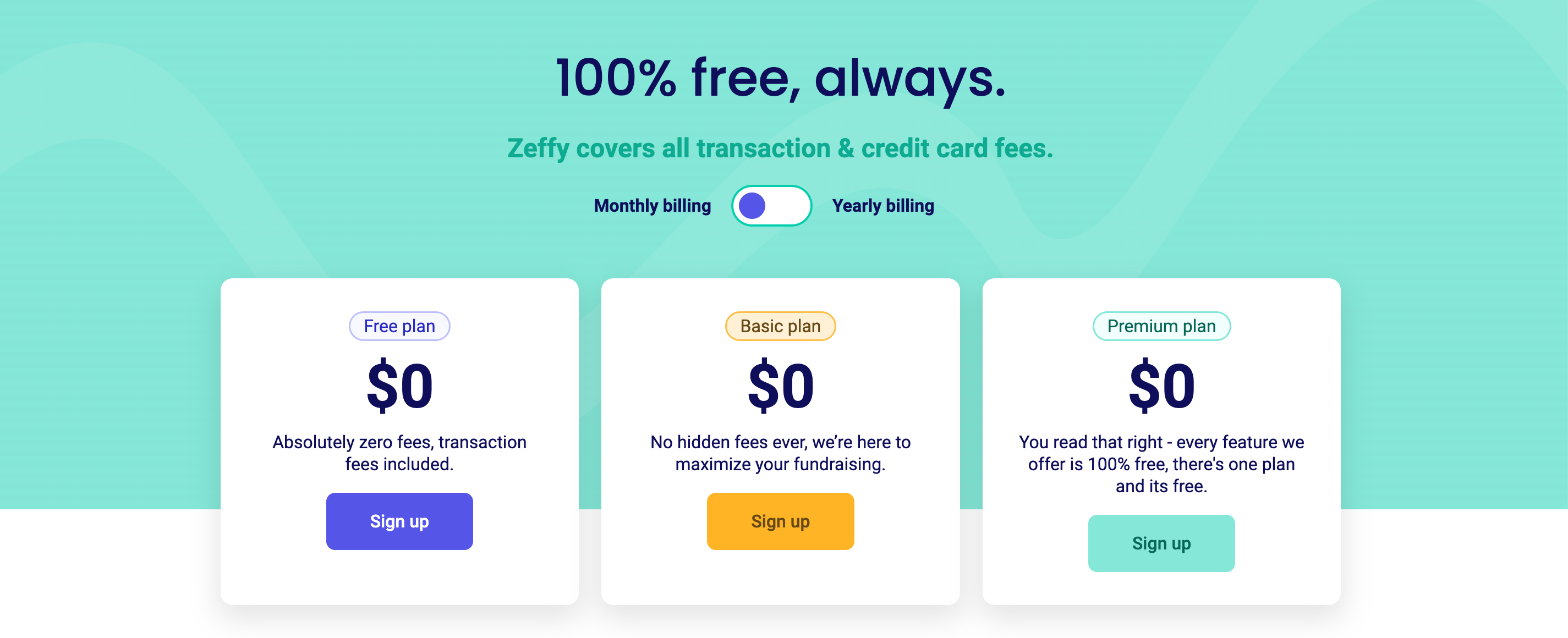

🇨🇦 Zeffy Proves That the Pay What You Want Pricing Model Can Work in Fintech Too As They Reach 50,000 Clients in the US

Montreal-based payment processor Zeffy has shown that the "pay-what-you-want" pricing model, famously used by Radiohead to sell their In Rainbows album (with fans paying an average of £2.90), can work in fintech as well. Zeffy uses a similar model by processing payments free of charge for nonprofits, while giving donors the option to contribute to the platform when making a donation, with the choice to pay nothing at all. While the company hasn’t revealed how much donors typically contribute, CEO François de Kerret announced in a LinkedIn post that Zeffy has processed $800 million for 50,000 U.S. nonprofits, saving them $40 million in fees.

Source: Global Fintech Insider

🇬🇧 The UK Changes Rules Protecting British Depositors in Favour of Goldman Sachs Owned Neobank Marcus

The UK government plans to raise the threshold for ringfencing, allowing the UK unit of neobank Goldman Sachs owned Marcus to expand its retail deposits beyond £25 billion (32.6 billion USD) without separating them from its riskier investment banking activities. Ringfencing rules, introduced after the 2008 financial crisis to protect consumer deposits, require banks to keep core retail services, like deposits and payments, separate from riskier operations. The new threshold of £35 billion (45.7 billion USD) will enable Marcus, which already have £21billion worth of deposits in the UK, to keep growing without facing additional costs linked to complying with the ringfencing rules.

Source: Financial Time

🇷🇺 Russia Proposes BRICS Payment System to Bypass SWIFT and US Dollar

Russia is proposing a new BRICS payment system to reduce reliance on the US dollar and bypass sanctions imposed by the US and its allies. This new payment system will be discussed at the annual BRICS summit that will take place in Kazan, Russia, on Oct. 22-24. This new SWIFT alternative could save BRICS nations up to $15 billion annually, would support multiple local currencies and would use distributed ledger technology (DLT) for cross-border transactions, eliminating intermediaries and credit risk. The proposal follows Russia’s exclusion from the SWIFT financial messaging network after its 2022 invasion of Ukraine.

Source: Bloomberg

🇺🇸 Financial Inclusion Fintech CapWay Collapse After Failing to Secure A New Banking Partner

CapWay, a fintech startup founded by Sheena Allen to offer a spending card associated with financial education to black communities in the US, has shut down. This news feels personal to me, as Sheena was the first fintech founder I met during the Queen City Fintech accelerator in 2017, when I was part of the same cohort with Hardbacon. She was highly confident, having already launched a successful app while still in college and she already mastered the power of storytelling when pitching CapWay. The fintech was an answer to a problem she witnessed while growing up in a black community in Mississippi, where most people were cashing out their checks at the grocery store. At least, that’s how she was pitching CapWay back in the days.

Despite joining Y Combinator in 2020 and raising $800,000, CapWay struggled after losing its banking partner. By then, the collapse of Synapse had led banking partners to require more capital from fintechs like hers and it made fundraising for a fintech without a banking partner even more difficult. In a LinkedIn post, Sheena wrote : “I feel strongly that there is still much work to be done in the financial inclusion space, so it won't be the last you hear of me in regard to fighting for economic equity.” Indeed, Sheena is already thinking about what fintech app she will launch and is open to become an entrepreneur-in-residence in a fintech VC.

Source: TechCrunch & Global Fintech Insider

🇸🇬 Singapore Bank Launches Disney Branded Cards and Accounts for Kids

Singapore-based bank OCBC has partnered with Disney to launch a unique banking experience across Southeast Asia, becoming the first regional bank to offer Disney, Pixar, Marvel, and Star Wars-inspired financial products and financial literacy content. This five-year collaboration aims to quadruple OCBC's new customer base by 2029, providing customers in Singapore, Malaysia, and Indonesia with special card designs, rewards programs that include Disney+ subscriptions, and exclusive merchandise. Starting October 20, OCBC will introduce the MyOwn Account, featuring Disney-themed financial literacy content aimed at young savers, including comics and activity sheets.

Source: Fintech Singapore

🇺🇸 The FTC Cracks Down on Hard to Cancel Recurring Subscriptions

The Federal Trade Commission (FTC) has introduced a new “click-to-cancel” rule requiring sellers to make canceling subscriptions as easy as signing up, addressing concerns about deceptive subscription practices. Effective 180 days after publication, these new rules could impact recurring subscription revenues generated by merchants and payment providers. Indeed, many subscriptions providers make it difficult to unsubscribe and are even paying Visa, Mastercard, and Amex for their credit card updater services, which allows merchants to continue charging customers even when their credit card numbers change.

Source: Washington Post

🇰🇪 Kenya To Monitor Crypto Transactions in Real Time to Fight Tax Evasion

The Kenya Revenue Authority (KRA) plans to introduce a real-time monitoring system for cryptocurrency transactions to curb tax evasion and capture earnings in the growing sector. With annual Kenya's crypto transactions reaching 2.4 trillion KES (18.6 million USD) per year, the Kenyan tax man seeks to regulate more effectively the four million Kenyans who deal in cryptocurrencies. The new system will integrate with crypto exchanges to track transaction details like date, time, and value, ensuring compliance with tax laws. The move comes as a parliamentary bill seeks to further regulate and tax crypto transactions and digital wallets in the country.

Source: TechCabal

Upcoming Fintech Events

🇺🇸 Money 20/20 will be held in Las Vegas on Oct. 27th to 30th ($3,999), with speakers such as Chris Britt, CEO of Chime and Daniela Amodei, president of Anthropic.

🇦🇪 The Binance Blockchain Week will take place in Dubai on Oct. 30-31 ($300), with speakers such as Jeremy Allaire, CEO of Circle and Eowyn Chen, CEO of Trust Wallet.

🇸🇬 The Singapore Fintech Festival will take place Nov. 6th to 8th, with speakers such as Kfir Godrich, Chief Innovation Officer at BlackRock and Richard Teng, CEO of Binance.

🇿🇦 The Africa Tech Festival will be held in Cape Town November 12-14 ($1,749), with speakers such as Kagiso Mothibi, CEO of MTN Fintech and Christian Kajeneri, director, payment systems at the National Bank of Rwanda.

🌐 The OpenFinity 2024 Expo will take place online on November 20-21 (free), with speakers such as Jane Barratt, Chief Advocacy Officer at MX and Roy Kao, board member at Open Finance Network Canada.

🇬🇧 Fintech Connect will be held in London on December 4-5 ($325), with speakers such as Zahra Gill, Financial Crime Strategy Lead at Starling Bank (!!!) and Anirudh Narla, Head of Product - Global Payments, Anti-Fraud & Wallet at Hopper.

🇺🇸 The Bank Automation Summit will be held in Austin on March 3-4, 2025 ($632.50), with speakers such as Michael Lehmbeck, CTO at BankUnited and Koren Picariello, head of generative AI strategy for Morgan Stanley Wealth Management.

Fintech’s Musical Chair

🇨🇦 Chris Ferron, former Sr Director of Global and NA Fintech Partnerships at Visa, has been appointed VP - Fintech Partnerships at Visa.

🇬🇧 William Reeve, former chairman of Nutmeg and current CEO of real estate software provider Goodlord, has been appointed as Chairman of the Board of Augmentum Fintech, Europe’s leading listed fintech fund, effective November 1, 2024.

🇺🇸 Ralph Hamers, former CEO of UBS, has joined AI-based digital wealth management startup Arta Finance as a senior advisor and investor.

🇰🇪 Rajeev Suri, former CEO of Nokia and Inmarsat, has been appointed Chairman of the Board at Kenyan fintech M-KOPA, effective December 1, 2024.

🇦🇺 Simon Keast, former US CFO of Zip Co, has been appointed CEO of Australian payment provider Ovanti to lead its US expansion, effective November 1, 2024.

🇺🇸 Mark Hara, former CEO of FloodFlash, has been appointed CEO of Atlanta-based insurtech startup Layr, succeeding founder Phillip Naples.

🇫🇷 Alexandre Schont, former Sales Director at RTB House, has been appointed VP Sales and member of the executive committee at iBanFirst, a global payments provider.

🇫🇷 William Gerlach, former France and UK Regional Director at iBanFirst, has been promoted to VP International Account Management & Dealing at iBanFirst.

🇸🇬 Yuri Mushkin, former Chief Risk Office at BlockFi, has been appointed Global Chief Risk Officer at Singapore-based cryptocurrency exchange OKX.

🇫🇷 Alexandra Chiaramonti, former VP and Managing Director for EMEA at GoCardless, has been appointed Managing Director of International Operations.

🇳🇱 Tim Rutten, former Chief of Staff at Backbase, a digital banking software provider, has been appointed Chief Marketing Officer at the same company.

🇫🇷 Axel Demazy, former COO at Jellysmack, has been appointed CEO of Spendesk, a French spend management platform, while founder Rodolphe Ardant remains as Chairman.

Have some fintech news you think I should include in the Global Fintech Insider newsletter or heard some rumours you’d like me to look into? Drop me an email at: jrbrault@protonmail.com